Calm before the StormCalm before the Storm - Bollinger Bands Volatility Indicator

What It Does

This indicator identifies and highlights periods of extremely low market volatility by analyzing Bollinger Bands distance. It uses percentile-based analysis to find the "quietest" market periods and highlights them with a gradient background, operating on the premise that low volatility periods often precede significant price movements.

How It Works

Volatility Measurement: Calculates the distance between Bollinger Bands upper and lower boundaries

Percentile Analysis: Analyzes the lowest X% of volatility periods over a configurable lookback period (default: lowest 40% over 200 bars)

Visual Highlighting: Uses gradient opacity to show volatility levels - the lower the volatility, the more opaque the background highlighting

Adaptive Threshold: Automatically calculates what constitutes "low volatility" based on recent market conditions

Who Should Use It

Primary Users:

Breakout Traders: Looking for consolidation periods that may precede significant moves

Options Traders: Seeking low implied volatility periods before volatility expansion

Swing Traders: Identifying accumulation/distribution phases before trend continuation or reversal

Range Traders: Spotting tight trading ranges for mean reversion strategies

Trading Styles:

Volatility-based strategies

Breakout and momentum trading

Options strategies (volatility plays)

Market timing approaches

When to Use It

Market Conditions:

Consolidation Phases: When price is moving sideways with decreasing volatility

Pre-Announcement Periods: Before earnings, economic data, or major events

Market Transitions: During shifts between trending and ranging markets

Low Volume Periods: When institutional participation is reduced

Strategic Applications:

Entry Timing: Wait for volatility compression before positioning for breakouts

Risk Management: Reduce position sizes during highlighted periods (anticipating volatility expansion)

Options Strategy: Sell premium during low volatility, buy during expansion

Multi-Timeframe Analysis: Combine with higher timeframe trends for confluence

Key Benefits

Objective Volatility Measurement: Removes subjectivity from identifying "quiet" markets

Adaptive Analysis: Automatically adjusts to current market conditions

Visual Clarity: Easy-to-interpret gradient highlighting

Customizable Sensitivity: Adjustable percentile thresholds for different trading styles

Best Used In Combination With:

Trend analysis tools

Support/resistance levels

Volume indicators

Momentum oscillators

This indicator is particularly valuable for traders who understand that periods of low volatility are often followed by periods of high volatility, allowing them to position ahead of potential significant price movements.

"Implied volatility" için komut dosyalarını ara

VIX Implied MovesKey Features:

Three Timeframe Bands:

Daily: Blue bands showing ±1σ expected move

Weekly: Green bands showing ±1σ expected move

30-Day: Red bands showing ±1σ expected move

Calculation Methodology:

Uses VIX's annualized volatility converted to specific timeframes using square root of time rule

Trading day convention (252 days/year)

Band width = Price × (VIX/100) ÷ √(number of periods)

Visual Features:

Colored semi-transparent backgrounds between bands

Progressive line thickness (thinner for shorter timeframes)

Real-time updates as VIX and ES prices change

Example Calculation (VIX=20, ES=5000):

Daily move = 5000 × (20/100)/√252 ≈ ±63 points

Weekly move = 5000 × (20/100)/√50 ≈ ±141 points

Monthly move = 5000 × (20/100)/√21 ≈ ±218 points

This indicator helps visualize expected price ranges based on current volatility conditions, with wider bands indicating higher market uncertainty. The probabilistic ranges represent 68% confidence levels (1 standard deviation) derived from options pricing.

Tomas' Financial Conditions Z Score"The indicator is a composite z-score comprised of the following four components (equally-weighted):

Credit spreads - ICE BofA High Yield Option Adjusted Spread (BAMLH0A0HYM2) and ICE BofA Corporate Index Option Adjusted Spread (BAMLC0A0CM)

Volatility indexes - VIX (S&P 500 implied volatility) and MOVE (US Treasury bond implied volatility)

I've got it set to a 160-day lookback period, which I think is roughly the best setting after some tinkering.

When the z-score is above zero, it throws a red signal - and when the z-score is below zero, it throws a green signal.

This indicator is a follow-on from the "traffic light financial conditions indicator" that I wrote a thread about a couple of months ago.

I moved on from that previous indicator because it is based on the Federal Reserve's NFCI, which is regularly revised, but I didn't take that into account at the time.

So not a great real-time indicator, if the signal can be subsequently revised in the opposite direction weeks later.

This new indicator is based on real-time market data, so there's no revisions, and it also updates daily, as opposed to weekly for the NFCI"

IV Rank/Percentile with Williams VIX FixDisplay IV Rank / IV Percentile

This indicator is based on William's VixFix, which replicates the VIX—a measure of the implied volatility of the S&P 500 Index (SPX). The key advantage of the VixFix is that it can be applied to any security, not just the SPX.

IV Rank is calculated by identifying the highest and lowest implied volatility (IV) values over a selected number of past periods. It then determines where the current IV lies as a percentage between these two extremes. For example, if over the past five periods the highest IV was 30%, the lowest was 10%, and the current IV is 20%, the IV Rank would be 50%, since 20% is halfway between 10% and 30%.

IV Percentile, on the other hand, considers all past IV values—not just the highest and lowest—and calculates the percentage of these values that are below the current IV. For instance, if the past five IV values were 30%, 10%, 11%, 15%, and 17%, and the current IV is 20%, the IV Rank remains at 50%. However, the IV Percentile is 80% because 4 out of the 5 past values (80%) are below the current IV of 20%.

VIX9D to VIX RatioVIX9D to VIX Ratio

The ratio > 1 can signal near-term fear > long-term fear (potential short-term stress).

The ratio < 1 implies long-term implied volatility is higher — more typical in calm markets.

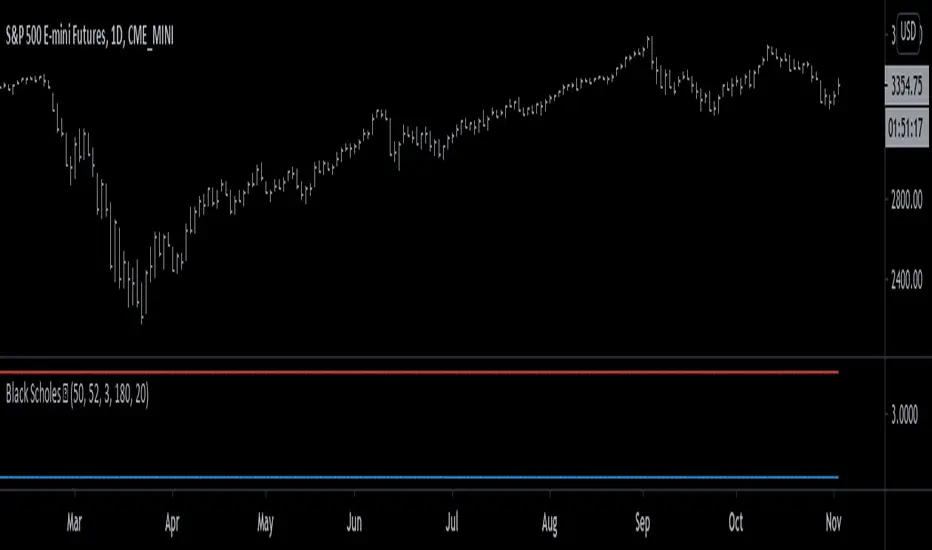

Black Scholes Model [racer8]This is the Black Scholes Model. This indicator tells you the prices of both a call option & a put option.

Input variables are spot price, strike price, risk free rate %, days to maturity, and implied volatility %.

This indicator was made generally for educational purposes.

By using this indicator, you will develop a better understanding of how options are priced.

This indicator was made to be as simple as possible so that the user can easily understand it.

I recreated the Black Scholes Model because there is very little scripts on TV that are based on the Black Scholes Model.

I am aware that are Black Scholes Model (BSM) scripts already on TV, but mine is not the same. Correct me if I'm wrong, but I don't think there is a BSM script out there yet that relies on the exact same inputs that mine does.

Why use this indicator?

If you don't already have your own IV indicator...

You can use this indicator to approximate the value of implied volatility %.

You already know every input variable except IV%, and you know the call & put option prices.

So put in the numbers for each input and put a random number between 0 to 100 into the IV% input to get the options prices.

Adjust that random number for IV% until the output (options prices) matches correctly with what you already know they are to be.

This is called the trial and error method.

On the other hand, if you already know all input variables including IV%. Then you can use this indicator to find the call & put options prices directly.

Hope this helps. Enjoy 🙂

Adaptive Bull Ratio Strategy█ Overview: Why This Strategy

Most option strategies fall into two traps:

They are too rigid: A "Call Ratio Spread" works great in slow markets but gets destroyed if the market rallies hard.

They are too simple: A simple "Buy Call" suffers from time decay (Theta) if the market chops sideways.

The Adaptive Bull Ratio Strategy solves both . It is a living strategy that "shifts gears" based on price action.

It is called "Adaptive" because it morphs its structure three times during a trade. It starts conservative to harvest Time Decay, but if the market explodes upwards, it "uncaps" itself to ride the trend aggressively.

█ The Entry Philosophy: Why Supertrend?

The default setting uses the Supertrend indicator as the trigger. This is intentional:

Volatility Awareness: Supertrend adapts to market noise using ATR. In high volatility, bands widen to prevent false entries.

Trend Confirmation: Since Phase 1 involves selling options, entering "too early" against a falling market is dangerous. Supertrend forces patience, waiting for a confirmed reversal (Close > Trend Line), ensuring the momentum is actually in your favor before you commit capital.

The "Drift" Benefit: This strategy excels in markets that "drift" upwards. Supertrend identifies these trends while filtering out short-term chop.

Flexibility with External Sources:

While Supertrend is the default, the strategy is designed to be flexible. You can enable the 'Enable External Source' option in the settings to plug in any custom indicator (e.g., Moving Averages, Parabolic SAR, or a proprietary trendline).

The Golden Rule for External Sources: The script interprets a Bullish Signal whenever your External Source line is below the Close price (Ext Source < Close).

Compatibility: As long as your custom indicator behaves like a support line in an uptrend (plotting below the candles), it will work seamlessly with this strategy's logic.

█ The "Long Only" Rationale: Avoiding the Volatility Trap

Why not trade this on the short side (Puts) during crashes?

The Volatility Trap (Vega Risk): In Bull markets, Implied Volatility (IV) usually drops, helping your sold options decay faster. In Bear markets, IV explodes (panic). Selling OTM Puts during a crash is dangerous as their value skyrockets, neutralizing gains.

Velocity Risk: Bear markets crash fast ("Elevator Down"). Prices can blow through adjustment levels faster than the strategy can safely roll down, causing slippage.

Structural Skew: OTM Puts are inherently more expensive. Buying expensive ITM Puts and selling expensive OTM Puts shifts the breakeven further away, making V-shape recoveries painful.

█ How It Works & Stands Out

This strategy actively transforms risk profiles based on market movement:

Phase 1: The "Safe" Start (Entry)

Setup: Initiates a Call Ratio Spread (Buy 2 ITM, Sell 4 OTM) + Protective Puts.

Logic: Profits from sideways drift or slow rallies via Time Decay (Theta). The sold options finance the trade.

Phase 2: The "Shift" (Adjustment Level 1)

Trigger: Market moves above Leg 2 (3 OTM Call).

Action: Rolls Up the position. Exits initial legs, enters new higher legs, and adds a Short Put to finance the roll.

Impact: Aggressive. You bet the trend is strong enough to support the added downside risk of the short put.

Phase 3: The "Uncap" (Adjustment Level 2)

Trigger: Market moves above Leg 3 (4 OTM Call).

Action: Exits all Sold Calls.

Impact: Uncaps profit potential. The trade becomes a Net Long position (Long Calls + Short Puts), allowing you to ride a massive rally without a ceiling.

Phase 4: The "Lock-In" (Optional Trail Adjustment)

Trigger: The market goes parabolic (price rises X levels above Leg 3, configurable in settings).

Action (If Enabled):

Call Adj: Exits the Phase 3 calls and buys fresh 1-OTM calls (Rolling Up to lock profits).

Put Adj: Exits all Put legs (Removing downside risk completely).

Impact: Maximum Safety. This phase is about "banking" the windfall from a massive rally and leaving a smaller, risk-free runner to capture any final extension.

█ How to Start: A Quick Setup Guide

Step 1: Map Expiry Dates

Manually input your trading expiry dates in Settings -> Expiry Management.

Format: YYYY-MM-DD (e.g., 2025-12-25). Strict adherence required for DhanHQ.

Step 2: Configure Symbol & Size

Exchange/Symbol: Enter NSE and NIFTY (or your ticker).

Lot Multiplier: Default is 1. Set to 2 to double all quantities (e.g., Buy 2 becomes Buy 4).

Step 3: Understand Visuals

Entry Window (Light Blue): Strategy is scanning for new trades.

Non-Entry Window (Dark Blue): Trading blocked (Day before Expiry & Expiry Day). Only management allowed.

Green Box: Valid Late Entry Zone.

Red Dashed Line: Invalidation Level (if price touches this, no late entry).

Fuchsia Line: Trigger level for Special Trail Adjustments (Phase 4).

IMPORTANT: Broker & Technology Heads-Up:

The alerts generated by this script ({"secret": "...", "alertType": "multi_leg_order"...}) are specifically formatted for the DhanHQ webhook structure.

Dhan Users: Plug-and-play.

Other Brokers: You need middleware (NextLevelBot, Quantiply) to parse the JSON.

█ Risk Disclaimer & Advice

Trading options involves substantial risk.

The Whipsaw Risk: In Phase 2, you are Long Calls and Short Puts. A sharp reversal causes losses on both sides.

Margin: Selling options requires significant margin. Keep a 15-20% cash buffer to handle adjustments instantly.

Testing: This strategy is optimized for NIFTY Weekly Options. Effectiveness on BankNifty or Stocks is untested and may require parameter tuning.

Advice:

Backtest: Use TradingView Replay.

Paper Trade: Run for at least one expiry cycle before live deployment.

Consult: Seek professional financial advice before trading.

Practical Tips for Smooth Execution

For a new trader deploying this system, these operational tips are vital:

Capital Buffer: Do not trade at your limit. Always keep 10-15% free cash in your broker account. Adjustments (specifically Phase 2, where you sell an extra Put) require additional margin instantly. If margin is short, the order fails, and your hedge breaks.

Liquidity Awareness : The script trades "Far Deep OTM" options (Leg 4) to reduce margin. On indices like Nifty/BankNifty, this is fine. On individual stocks, these deep strikes might be illiquid. Check the option chain volume before deploying on stocks.

Trust the Process (but Verify) : While the algo drives, you are the pilot.

Check your API connection every morning.

Ensure the "Entry Window" background color on the chart matches your real-world date.

Verify that your broker executed all legs of a multi-leg order (partial fills are rare but possible).

The "Human" Stop: If major news breaks (e.g., unexpected election results, war announcements), volatility can expand faster than any algo can react. It is acceptable—and smart—to pause the strategy during known "Black Swan" events or earnings releases.

█ Timeframe Selection: The 30-Minute Standard

Critical Requirement: This indicator must be applied to a 30-minute chart.

Why?

Noise Filtering: The Supertrend logic is tuned to capture multi-day trends. Lower timeframes (5m, 15m) are full of "noise"—random fluctuations that look like trend changes but aren't.

Execution Logic (The Hybrid Engine): The script has a built-in "Dual Timeframe" architecture.

Decision Layer (30m): Uses the chart timeframe to decide when to be Bullish or Bearish.

Execution Layer (5m): Internally fetches 5-minute data to manage the how (Adjustments, Late Entries, and precise invalidation).

The Risk of Lower Timeframes: If you run the main chart on 5-minutes, you destroy this hierarchy. You will get too many signals, pay too much brokerage, and the internal logic may behave erratically.

Recommendation: Always keep your TradingView chart interval at 30m. Do not switch to lower timeframes expecting "faster" signals; you will likely just get "false" signals.

█ Testing Scope, Feedback

⚠️ Important Note on Asset Classes:

This strategy logic and the associated strike step calculations have been rigorously tested ONLY on NIFTY Index Options with Weekly Expiry.

BankNifty / Sensex / FinNifty: The volatility characteristics (ATR) and strike intervals of these instruments differ significantly from NIFTY. The effectiveness of this strategy on these other scripts has not been verified and may require different parameter tuning (e.g., strike_step or ATR Length).

Stocks: Individual stock options often lack the liquidity required for the "Deep OTM" legs, leading to potential execution failures.

We encourage traders to backtest this logic on other indices and share their findings! If you find a robust parameter set for BankNifty or observe unique behaviors on other scripts, please let us know in the comments below so we can improve the algorithm for everyone. Your feedback is appriciated.

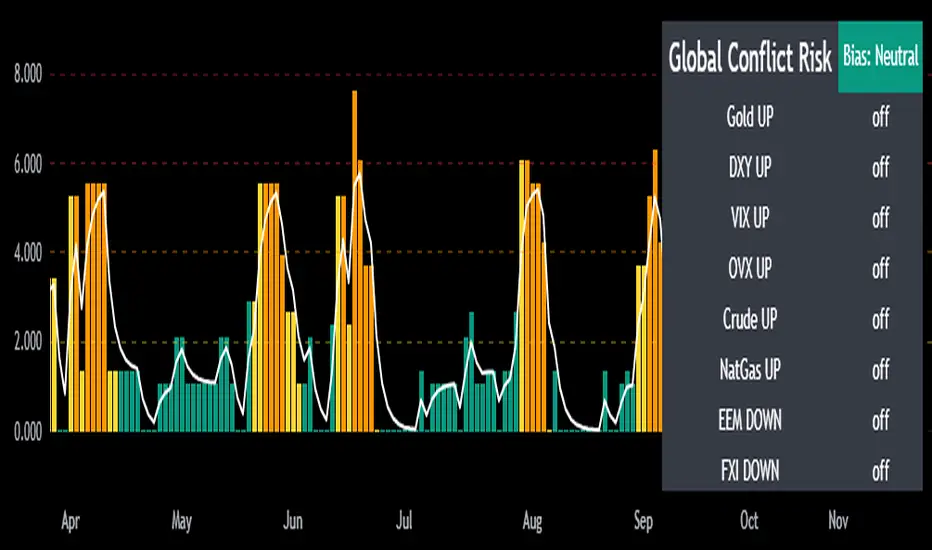

Mongoose Global Conflict Risk Index v1Overview

The Mongoose Global Conflict Risk Index v1 is a multi-asset composite indicator designed to track the early pricing of geopolitical stress and potential conflict risk across global markets. By combining signals from safe havens, volatility indices, energy markets, and emerging market equities, the index provides a normalized 0–10 score with clear bias classifications (Neutral, Caution, Elevated, High, Shock).

This tool is not predictive of headlines but captures when markets are clustering around conflict-sensitive assets before events are widely recognized.

Methodology

The indicator calculates rolling rate-of-change z-scores for eight conflict-sensitive assets:

Gold (XAUUSD) – classic safe haven

US Dollar Index (DXY) – global reserve currency flows

VIX (Equity Volatility) – S&P 500 implied volatility

OVX (Crude Oil Volatility Index) – energy stress gauge

Crude Oil (CL1!) – WTI front contract

Natural Gas (NG1!) – energy security proxy, especially Europe

EEM (Emerging Markets ETF) – global risk capital flight

FXI (China ETF) – Asia/China proxy risk

Rules:

Safe havens and vol indices trigger when z-score > threshold.

Energy triggers when z-score > threshold.

Risk assets trigger when z-score < –threshold.

Each trigger is assigned a weight, summed, normalized, and scaled 0–10.

Bias classification:

0–2: Neutral

2–4: Caution

4–6: Elevated

6–8: High

8–10: Conflict Risk-On

How to Use

Timeframes:

Daily (1D) for strategic signals and early warnings.

4H for event shocks (missiles, sanctions, sudden escalations).

Weekly (1W) for sustained trends and macro build-ups.

What to Look For:

A single trigger (for example, Gold ON) may be noise.

A cluster of 2–3 triggers across Gold, USD, VIX, and Energy often marks early stress pricing.

Elevated readings (>4) = caution; High (>6) = rotation into havens; Shock (>8) = market conviction of conflict risk.

Practical Application:

Monitor as a heatmap of global stress.

Combine with fundamental or headline tracking.

Use alert conditions at ≥4, ≥6, ≥8 for systematic monitoring.

Notes

This indicator is for informational and educational purposes only.

It is not financial advice and should be used in conjunction with other analysis methods.

Volatility Strategy 01a quantitative volatility strategy (especially effective in trend direction on the 15min chart on the s&p-index)

the strategy is a rule-based setup, which dynamically adapts to the implied volatility structure (vx1!–vx2!)

context-dependent mean reversion strategy based on multiple timeframes in the vix index

a signal is provided under following conditions:

1. the vvix/vix spread has deviated significantly beyond one standard deviation

2. the vix is positioned above or below 3 moving averages on 3 minor timeframes

3. the trade direction is derived from the projected volatility regime, measured via vx1! and vx2! (cboe)

India VIXThe VIX chart represents the Volatility Index, commonly referred to as the "Fear Gauge" of the stock market. It measures the market's expectations of future volatility over the next 30 days, based on the implied volatility of NSE index options. The VIX is often used as an indicator of investor sentiment, reflecting the level of fear or uncertainty in the market.

Here’s a breakdown of what you might observe on a typical VIX chart:

VIX Value: The y-axis typically represents the VIX index value, with higher values indicating higher levels of expected market volatility (more fear or uncertainty), and lower values signaling calm or stable market conditions.

VIX Spikes: Large spikes in the VIX often correspond to market downturns or periods of heightened uncertainty, such as during financial crises or major geopolitical events. A high VIX is often associated with a drop in the stock market.

VIX Drops: A decline in the VIX indicates a reduction in expected market volatility, usually linked with periods of market calm or rising stock prices.

Trend Analysis: Technical traders might use moving averages or other indicators on the VIX chart to assess the potential for future market movements.

Inverse Relationship with the Stock Market: Typically, there is an inverse correlation between the VIX and the stock market. When stocks fall sharply, volatility increases, and the VIX tends to rise. Conversely, when the stock market rallies or remains stable, the VIX tends to fall.

A typical interpretation would be that when the VIX is low, the market is relatively stable, and when the VIX is high, the market is perceived to be uncertain or volatile.

CSP Key Level Finder This script is designed for option sellers, particularly those using strategies like cash-secured puts (CSPs), to help automate the process of identifying key levels in the market. The core functionality is to calculate a specific price level where a 5% return can be achieved based on the historical volatility of the underlying asset. This level is visually plotted on a chart to guide traders in making more informed decisions without manually calculating the thresholds themselves.

The script incorporates implied volatility (IV) data to determine the volatility rank of the asset and calculates historical volatility (HV) based on price movements. These volatility measures help assess market conditions. The resulting key level is drawn as a line on the chart, along with a label that includes relevant information about volatility, making it easier for traders to evaluate potential option selling strategies.

Additionally, the script includes user input options, allowing users to control when to display the key level on the chart, offering flexibility based on individual needs. Overall, the script provides a visual aid for option sellers to streamline the process of identifying attractive entry points.

MOVE/VXTLT CorrelationMany know of the VIX for equity trading. Yet, many are unaware that there is the same kind of volatility measure for trading bonds, called the MOVE Index.

"The Merrill Lynch Option Volatility Estimate (MOVE) Index is a yield curve weighted index of the normalized implied volatility on 1-month Treasury options which are weighted on the 2, 5, 10, and 30 year contracts."

With this script one can see the the correlation and divergences between bonds and its volatility measure to make educated decisions in trading or hedging.

The idea of this script comes from NicTheMajestic.

σ-Based SL/TP (Long & Short). Statistical Volatility (Quant Upgrade of ATR)

Instead of ATR’s simple moving average, use standard deviation of returns (σ), realized volatility, or implied volatility (options data).

SL = kσ, TP = 2kσ (customizable).

Why better than ATR: more precise reflection of actual distribution tails, not just candle ranges.

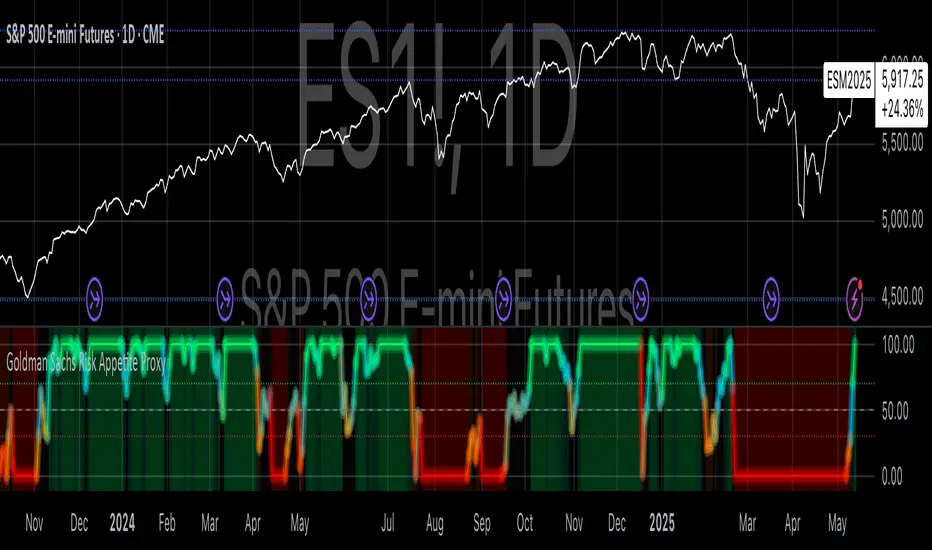

Goldman Sachs Risk Appetite ProxyRisk appetite indicators serve as barometers of market psychology, measuring investors' collective willingness to engage in risk-taking behavior. According to Mosley & Singer (2008), "cross-asset risk sentiment indicators provide valuable leading signals for market direction by capturing the underlying psychological state of market participants before it fully manifests in price action."

The GSRAI methodology aligns with modern portfolio theory, which emphasizes the importance of cross-asset correlations during different market regimes. As noted by Ang & Bekaert (2002), "asset correlations tend to increase during market stress, exhibiting asymmetric patterns that can be captured through multi-asset sentiment indicators."

Implementation Methodology

Component Selection

Our implementation follows the core framework outlined by Goldman Sachs research, focusing on four key components:

Credit Spreads (High Yield Credit Spread)

As noted by Duca et al. (2016), "credit spreads provide a market-based assessment of default risk and function as an effective barometer of economic uncertainty." Higher spreads generally indicate deteriorating risk appetite.

Volatility Measures (VIX)

Baker & Wurgler (2006) established that "implied volatility serves as a direct measure of market fear and uncertainty." The VIX, often called the "fear gauge," maintains an inverse relationship with risk appetite.

Equity/Bond Performance Ratio (SPY/IEF)

According to Connolly et al. (2005), "the relative performance of stocks versus bonds offers significant insight into market participants' risk preferences and flight-to-safety behavior."

Commodity Ratio (Oil/Gold)

Baur & McDermott (2010) demonstrated that "gold often functions as a safe haven during market turbulence, while oil typically performs better during risk-on environments, making their ratio an effective risk sentiment indicator."

Standardization Process

Each component undergoes z-score normalization to enable cross-asset comparisons, following the statistical approach advocated by Burdekin & Siklos (2012). The z-score transformation standardizes each variable by subtracting its mean and dividing by its standard deviation: Z = (X - μ) / σ

This approach allows for meaningful aggregation of different market signals regardless of their native scales or volatility characteristics.

Signal Integration

The four standardized components are equally weighted and combined to form a composite score. This democratic weighting approach is supported by Rapach et al. (2010), who found that "simple averaging often outperforms more complex weighting schemes in financial applications due to estimation error in the optimization process."

The final index is scaled to a 0-100 range, with:

Values above 70 indicating "Risk-On" market conditions

Values below 30 indicating "Risk-Off" market conditions

Values between 30-70 representing neutral risk sentiment

Limitations and Differences from Original Implementation

Proprietary Components

The original Goldman Sachs indicator incorporates additional proprietary elements not publicly disclosed. As Goldman Sachs Global Investment Research (2019) notes, "our comprehensive risk appetite framework incorporates proprietary positioning data and internal liquidity metrics that enhance predictive capability."

Technical Limitations

Pine Script v6 imposes certain constraints that prevent full replication:

Structural Limitations: Functions like plot, hline, and bgcolor must be defined in the global scope rather than conditionally, requiring workarounds for dynamic visualization.

Statistical Processing: Advanced statistical methods used in the original model, such as Kalman filtering or regime-switching models described by Ang & Timmermann (2012), cannot be fully implemented within Pine Script's constraints.

Data Availability: As noted by Kilian & Park (2009), "the quality and frequency of market data significantly impacts the effectiveness of sentiment indicators." Our implementation relies on publicly available data sources that may differ from Goldman Sachs' institutional data feeds.

Empirical Performance

While a formal backtest comparison with the original GSRAI is beyond the scope of this implementation, research by Froot & Ramadorai (2005) suggests that "publicly accessible proxies of proprietary sentiment indicators can capture a significant portion of their predictive power, particularly during major market turning points."

References

Ang, A., & Bekaert, G. (2002). "International Asset Allocation with Regime Shifts." Review of Financial Studies, 15(4), 1137-1187.

Ang, A., & Timmermann, A. (2012). "Regime Changes and Financial Markets." Annual Review of Financial Economics, 4(1), 313-337.

Baker, M., & Wurgler, J. (2006). "Investor Sentiment and the Cross-Section of Stock Returns." Journal of Finance, 61(4), 1645-1680.

Baur, D. G., & McDermott, T. K. (2010). "Is Gold a Safe Haven? International Evidence." Journal of Banking & Finance, 34(8), 1886-1898.

Burdekin, R. C., & Siklos, P. L. (2012). "Enter the Dragon: Interactions between Chinese, US and Asia-Pacific Equity Markets, 1995-2010." Pacific-Basin Finance Journal, 20(3), 521-541.

Connolly, R., Stivers, C., & Sun, L. (2005). "Stock Market Uncertainty and the Stock-Bond Return Relation." Journal of Financial and Quantitative Analysis, 40(1), 161-194.

Duca, M. L., Nicoletti, G., & Martinez, A. V. (2016). "Global Corporate Bond Issuance: What Role for US Quantitative Easing?" Journal of International Money and Finance, 60, 114-150.

Froot, K. A., & Ramadorai, T. (2005). "Currency Returns, Intrinsic Value, and Institutional-Investor Flows." Journal of Finance, 60(3), 1535-1566.

Goldman Sachs Global Investment Research (2019). "Risk Appetite Framework: A Practitioner's Guide."

Kilian, L., & Park, C. (2009). "The Impact of Oil Price Shocks on the U.S. Stock Market." International Economic Review, 50(4), 1267-1287.

Mosley, L., & Singer, D. A. (2008). "Taking Stock Seriously: Equity Market Performance, Government Policy, and Financial Globalization." International Studies Quarterly, 52(2), 405-425.

Oppenheimer, P. (2007). "A Framework for Financial Market Risk Appetite." Goldman Sachs Global Economics Paper.

Rapach, D. E., Strauss, J. K., & Zhou, G. (2010). "Out-of-Sample Equity Premium Prediction: Combination Forecasts and Links to the Real Economy." Review of Financial Studies, 23(2), 821-862.

Normal Distribution CurveThis Normal Distribution Curve is designed to overlay a simple normal distribution curve on top of any TradingView indicator. This curve represents a probability distribution for a given dataset and can be used to gain insights into the likelihood of various data levels occurring within a specified range, providing traders and investors with a clear visualization of the distribution of values within a specific dataset. With the only inputs being the variable source and plot colour, I think this is by far the simplest and most intuitive iteration of any statistical analysis based indicator I've seen here!

Traders can quickly assess how data clusters around the mean in a bell curve and easily see the percentile frequency of the data; or perhaps with both and upper and lower peaks identify likely periods of upcoming volatility or mean reversion. Facilitating the identification of outliers was my main purpose when creating this tool, I believed fixed values for upper/lower bounds within most indicators are too static and do not dynamically fit the vastly different movements of all assets and timeframes - and being able to easily understand the spread of information simplifies the process of identifying key regions to take action.

The curve's tails, representing the extreme percentiles, can help identify outliers and potential areas of price reversal or trend acceleration. For example using the RSI which typically has static levels of 70 and 30, which will be breached considerably more on a less liquid or more volatile asset and therefore reduce the actionable effectiveness of the indicator, likewise for an asset with little to no directional volatility failing to ever reach this overbought/oversold areas. It makes considerably more sense to look for the top/bottom 5% or 10% levels of outlying data which are automatically calculated with this indicator, and may be a noticeable distance from the 70 and 30 values, as regions to be observing for your investing.

This normal distribution curve employs percentile linear interpolation to calculate the distribution. This interpolation technique considers the nearest data points and calculates the price values between them. This process ensures a smooth curve that accurately represents the probability distribution, even for percentiles not directly present in the original dataset; and applicable to any asset regardless of timeframe. The lookback period is set to a value of 5000 which should ensure ample data is taken into calculation and consideration without surpassing any TradingView constraints and limitations, for datasets smaller than this the indicator will adjust the length to just include all data. The labels providing the percentile and average levels can also be removed in the style tab if preferred.

Additionally, as an unplanned benefit is its applicability to the underlying price data as well as any derived indicators. Turning it into something comparable to a volume profile indicator but based on the time an assets price was within a specific range as opposed to the volume. This can therefore be used as a tool for identifying potential support and resistance zones, as well as areas that mark market inefficiencies as price rapidly accelerated through. This may then give a cleaner outlook as it eliminates the potential drawbacks of volume based profiles that maybe don't collate all exchange data or are misrepresented due to large unforeseen increases/decreases underlying capital inflows/outflows.

Thanks to @ALifeToMake, @Bjorgum, vgladkov on stackoverflow (and possibly some chatGPT!) for all the assistance in bringing this indicator to life. I really hope every user can find some use from this and help bring a unique and data driven perspective to their decision making. And make sure to please share any original implementaions of this tool too! If you've managed to apply this to the average price change once you've entered your position to better manage your trade management, or maybe overlaying on an implied volatility indicator to identify potential options arbitrage opportunities; let me know! And of course if anyone has any issues, questions, queries or requests please feel free to reach out! Thanks and enjoy.

VIX MTF MomentumSweet little momentum gadget to track the VIX Index.

What is the VIX?

The CBOE S&P 500 Volatility Index (VIX) is known as the 'Fear Index' which can measure how worried traders are that the S&P 500 might suddenly drop within the next 30 days.

When the VIX starts moving higher, it is telling you that traders are getting nervous. When the VIX starts moving lower, it is telling you that traders are gaining confidence.

VIX calculation?

The Chicago Board of Options Exchange Market Volatility Index (VIX) is a measure of implied volatility (Of the S&P 500 securities options), based on the prices of a basket of S&P 500 Index options with 30 days to expiration.

How to use:

If VIX Momentum is above 0 (RED) traders are getting nervous.

If VIX Momentum is below 0 (GREEN) traders are gaining confidence.

Follow to get updates and new scripts: www.tradingview.com

Risk RangeThis indicator creates risk ranges using implied volatility (VIX) or historical volatility, skewness ( Cboe SKEW or estimate ) and kurtosis.

Realized Variables for Options ComparisonThese variables can be used in comparison with the implied volatility of options.

Variables:

Realized Volatility

mathematical notation lowercase 'sigma'

Realized Variance

mathematical notation lowercase 'sigma' squared

Realized Beta

mathematical notation lowercase 'beta'

Timeframes:

Yearly = 250 or 365

Quarterly = 50 or 90

Monthly = 20 or 30

Important Note:

Options Contract Expiry = barmerge.lookahead_on

"Merge strategy for the requested data position. Requested barset is merged with current barset in the order of sorting bars by their opening time. This merge strategy can lead to undesirable effect of getting data from "future" on calculation on history. This is unacceptable in backtesting strategies, but can be useful in indicators."

[ All other timeframes barmerge.lookahead is disabled.

Buying Opportunity Score V2.2Buying Opportunity Indicator V2.2

What This Indicator Does

This indicator identifies potential buying opportunities during market fear and pullbacks by combining multiple technical signals into a single composite score (0-100). Higher scores indicate more fear/oversold conditions are present simultaneously.

Why These Components?

Market bottoms typically occur when multiple fear signals align. This indicator combines five complementary measurements that each capture different aspects of market stress:

1. VIX Level (30 points) - Measures implied volatility/fear. VIX spikes during selloffs as traders buy protection. Thresholds based on historical percentiles (VIX 25+ is ~85th percentile historically).

2. Price Drawdown (30 points) - Distance from 52-week high. Larger drawdowns create better risk/reward for mean reversion entries. A 10%+ drawdown from highs historically presents better entry points than buying at all-time highs.

3. RSI 14 (12 points) - Classic momentum oscillator measuring oversold conditions. RSI below 30 indicates short-term selling exhaustion.

4. Bollinger Band Position (13 points) - Statistical measure of price extension. Price below the lower band (2 standard deviations) indicates statistically unusual weakness.

5. VIX Timing (15 points) - Bonus points when VIX is declining from a recent peak. This helps avoid catching falling knives by waiting for fear to subside.

How The Score Works

- Each component contributes points based on severity

- Components are weighted by predictive value from historical analysis

- Score of 70+ means multiple fear signals are present

- Score of 80+ means extreme fear across most components

How To Use

1. Apply to SPY, QQQ, or IWM on daily timeframe

2. Monitor the Current Score in the statistics table

3. Scores below 50 = normal conditions, no action needed

4. Scores 60-69 = elevated fear, monitor closely

5. Scores 70+ = consider entering long positions

6. Scores 80+ = strongest historical entry points

Important Limitations

- This is a research tool, not financial advice

- Past patterns may not repeat in the future

- Signals are infrequent (typically 2-4 per year reaching 70+)

- Works best on broad market ETFs; not validated for individual stocks

- Always use proper position sizing and risk management

- The indicator identifies conditions that have historically been favorable, but cannot predict future returns

Statistics Table

The table shows:

- Current Score with context message

- Chart Results: Rolling 1Y/3Y/5Y statistics from your loaded chart data

Alerts

Multiple alert options available for different score thresholds.

Open Source

Code is fully visible for review and educational purposes.

FF calculation Saptarshi ChatterjeeForward factor (in options contexts) measures implied volatility (IV) for a future period between two expirations, like from 30 DTE (days to expiry) front-month to 60 DTE back-month options.

This indicator calculates the FORWARD FACTOR(FF) using 2 IVs of 2 DTEs.

+ve value means front DTE is rich in premium and back expiry is cheap.

-ve value means front DTE IV is cheap and 2nd DTE is expensive

we can use this term structure disbalance to trade calendar spreads with edge.

5EMA BollingerBand Nifty Stock Scanner

What ?

We all heard about (well: over-heard) 5-EMA strategy. Which falls into the broader category of mean reversal type of trading setup.

What is mean reversal?

Price (or any time series, in fact) tries to follow a mean . Whenever price diverges from the mean it tries to meet it back.

It is empirically observed by some traders (I honestly don't know who first time observed it) that in Indian context specially, 5 Exponential Moving Average (5-EMA) works pretty good as that mean.

So whenever price moves away from that 5-EMA, it ultimately comes back and attain total nirvana :) Means: if price moved way higher than the 5EMA without touching it, then price will correct to meet it's 5-EMA and if price moved way lower, it will be uplifted to meet it's 5-EMA. Funny - but it works !

Now there are already enough social media coverage on this 5-EMA strategy/setup. Even TradingView has some excellent work done on these setups. Kudos to all those great souls.

So when we came to know about this, we were thinking what we should do for the community. Because it is well cover topic (specially in Indian context). Also, there are public indicators.

Then we thought why not come up with a scanner which will scan all the Nifty-50 constituent stocks and find out on the fly, real-time which all stocks are matching this 5-EMA setup and causing a Buy/Sell trade recommendation.

Hence here we are with the first version of our first scanner on the 5EMA setup (well it has some more masala than merely a 5-EMA setup).

Why?

Parts of why is already covered up.

Now instead of blindly following 5-EMA setup, we added the Bollinger band as well. Again: it's also not new. There are enough coverage in social media about the 5-EMA+BB strategy/setup. We mercilessly borrowed from all of these.

Suppose you have an indicator.

Now you apply the indicator in your chart. And then you need to (rock) and roll through your watchlist of Nifty-50 stocks (note: TradingView has no default watchlist of Nifty-50 stock by default - you have to create one custom watchlist to list all manually) to find out which all are matching the setup, need to take a note about the trade recomendations (entry, SL, target) and other stuffs like VWAP, Volume, volatility (Bollinger Band Width).

Not any more.

This scanner will track all the Nifty-50 stocks (technically: 40 stocks other than Banking stocks) and provide which one to Buy or Sell (if any), what's the entry, SL, target, where is the VWAP of the day, what's the picture in volume (high, low, rising, falling) and the implied volatility (using Bolling band width). Also it has a naive alerting mechanism as well.

In fact the code is there to monitor the (Future) OI also and all the OI drama (OI vs price and all the 4 stuffs like long build up, long unwinding, short covering, short buildup). But unfortunately, due to some limitations of the TradingView (that one can not monitor more than 40 `ta.security` call) we have to comment out the code. If you wish you can monitor only 20 stocks and enable the OI monitoring also (20 for stocks + 20 for their OI monitoring .. total 40 `ta.security` call).

How?

To know the divergence from 5-EMA we just check if the high of the candle (on closing) is below the 5-EMA. Then we check if the closing is inside the Bollinger Band (BB). That's a Buy signal. SL: low of the candle, T: middle and higher BB.

Just opposite for selling. 5-EMA low should be above 5-EMA and closing should be inside BB (lesser than BB higher level). That's a Sell signal. SL: high of the candle, T: middle and lower BB.

Along with we compare the current bar's volume with the last-20 bar VWMA (volume weighted moving average) to determine if the volume is high or low.

Present bar's volume is compared with the previous bar's volume to know if it's rising or falling.

VWAP is also determined using `ta.vwap` built-in support of TradingView.

The Bolling Band width is also notified, along with whether it is rising or falling (comparing with previous candle).

Simple, but effective.

Customization

As usual the EMA setup (5 default), the BB setup (20 SMA with 1.5 standard deviation), we provided option wherther to include or exclude BB role in the 5-EMA setup (as we found out there are two schools of thought .. some people use BB some don't. Lets make all happy :))

We also provide options to choose other symbols using Settings if they wish so. We have the default 40 non banking Nifty stocks (why non-banking? - Bank Nifty is in ATH :) .. enough :)). But if user wishes can monitor others too (provided the symbol is there in TradingView).

Although we strongly recommend the timeframe as 30 minutes , you can choose what's fit you most.

The output of the scanner is a table. By default the table is placed in the right-bottom (as we are most comfortable with that). However you can change per your wish. We have the option to choose that.

What is unique in it ?

This is more of an indicator. This is a scanner (of Nifty-50 stocks). So you can apply (our recommendation is in 30m timeframe) it to any chart (does not matter which chart it is) and it will show every 30 mins (which is also configurable) which all stocks (along with trade levels) to Buy and Sell according to the setup.

It will ease your trading activity.

You can concentrate only on the execution, the filtering you can leave it to this one.

Limitations

There is a build in limitation of the TradingView platform is that one can call only upto 40 securities API. Not beyond that. So naturally we are constraint by that. Otherwise we could monitor 190 Nifty F&O stocks itself.

30m is the recommended timeframe. In very lower (say 5m) this script tends to go out of heap (out of memory). Please note that also.

How to trade using this?

Put any chart in 30m (recommended) timeframe.

Apply this screener from Indicators (shortcut to launch indicators is just type / in your keyboard).

This will provide the Buy (shown in green color) or Sell (shown in red color) recommendations in a table, at every 30m candle closing.

Note the volume and BB width as well.

Wait for at least 2 5-minutes candles to close above/below the recommended level .

Take the trade with the SL and target mentioned.

Mentions

@QuantNomad. The whole implementation concept we mercilessly borrowed from him, even some of his code snippet we took it (after asking him through one of his videos comment section and seeking explicit permission which he readily granted within an hour). Thank You sir @QuantNomad. Indebted to you.

Monika (Rawat) ji: for reviewing, correcting, providing real time examples during live market hours, often compromising her own trading activities, about the effectiveness and usefulness of this setup. Thank You madam ji. Indebted to you.

There are innumerable contents in social media about this. Don't even know whom all we checked. Thanks to all of them.

Happy Trading (in stocks - isn't enough of Indices already?)

Disclaimer

This piece of software does not come up with any warrantee or any rights of not changing it over the future course of time.

We are not responsible for any trading/investment decision you are taking out of the outcome of this indicator.

Options Price CalculatorIn the team, we continue to explore and expand the boundaries of TradingView.

For now, there is not much an options trader can do with options in TradingView.

We wanted to change that and created a simple option pricer.

You can set up in parameters a set of strikes, implied volatility, and days to expiry.

The indicators will take a risk-free rate from US01Y and the underlying price from your current chart.

It will compute prices and greeks for both put and call options.

Thanks to @MUQWISHI for helping code it.

Disclaimer

Please remember that past performance may not indicate future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

VIX Rule of 16There’s an interesting aspect of VIX that has to do with the number 16. (approximately the square root of the number of trading days in a year).

In any statistical model, 68.2% of price movement falls within one standard deviation (1 SD ). The rest falls into the “tails” outside of 1 SD .

When you divide any implied volatility (IV) reading (such as VIX ) by 16, the annualized number becomes a daily number

The essence of the “rule of 16.” Once you get it, you can do all sorts of tricks with it.

If the VIX is trading at 16, then one-third of the time, the market expects the S&P 500 Index (SPX) to trade up or down by more than 1% (because 16/16=1). A VIX at 32 suggests a move up or down of more than 2% a third of the time, and so on.

• VIX of 16 – 1/3 of the time the SPX will have a daily change of at least 1%

• VIX of 32 – 1/3 of the time the SPX will have a daily change of at least 2%

• VIX of 48 – 1/3 of the time the SPX will have a daily change of at least 3%